Household debt relief programs by the CCRS

Based on the 「Micro Credit Support Act」, Household debt relief programs by the CCRS helps you manage your debts in financial institutions that signed the Agreement on debt relief support.

Benefits of a Household debt relief programs by the CCRS

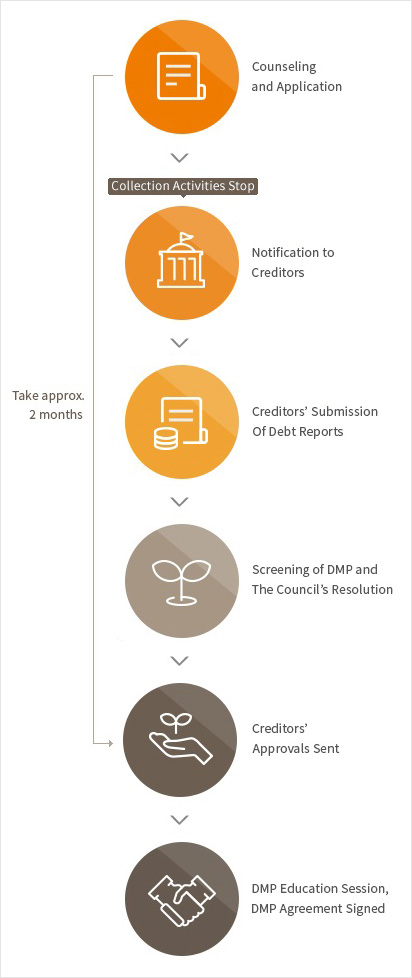

- From the next day of application of the debt relief program, creditors would stop any collection activities.

- There is almost no cost except the application fee of KRW 50,000.

- We consolidate all your unsecured debts in our member financial institutions so that you can make one lump sum payment each month.

- Our direct arrangement with financial institutions enables a speedy process.

- Our application procedure and necessary documents are simple and you can apply at your first visit.

- Online application is available for those who cannot visit in person.

Application Procedure

Individual workout by the CCRS

Individual workout by the CCRS

| Criteria |

Details of Support |

| Eligibility |

- In order to apply, you need …

- to have a payment which is more than three months overdue, and

- debt of which total amount is no more than KRW 1.5 billion, and unsecured debt is no more than KRW 1 billion, while secured debt is no more than KRW 500 million, and

- income which is no less than the minimum living cost or are recognized by the council that you can repay your debt.

|

| Reduction and discharge of debt |

- The interest and overdue interest are fully exempted.

- Principal reduction for the financial institution’s bad debts(Up to 70%)

- principal reduction up to 90% for socially vulnerable class

|

| Extension of Repayment Period |

- A maximum of 8 years

- A maximum of 10 years for those whose income is no more than the next lowest income bracket

|

| Postponement of Payments |

- You may postpone your payments up to 2 years considering the type of your loan, amount of total debt, ability to repay, your collateral and credit records.

|

Pre-workout by the CCRS

Pre-workout by the CCRS

| Criteria |

Details of Support |

| Eligibility |

- In order to apply, you need …

- to have a payment which is more than 30 days overdue, but less than 91 days overdue(if your overdue period is between one and 30 days, your yearly income should be no more than KRW 40 million, and accumulated overdue days within one year from the application day should be no less than 30 days), and

- debt of which total amount is no more than KRW 1.5 billion, and unsecured debt is no more than KRW 1 billion, while secured debt is no more than KRW 500 million, and

- newly created(created within 6 months from the application day) debts no more than 30% of the total debt

- You created a new debt equal to or less than 30% of the total debt amount within the last 6 months from the date of application

|

| Interest Rate Reduction |

- The overdue interest is fully exempted.

- Up to 50% of the contracted interest rate

- The reduced yearly interest rate is a maximum of 10 percent, and a minimum of 5 percent, and if contracted rate is less than 5 percent, the rate is applied.

|

|

Extension of Repayment period

|

|

| Postponement of Payments |

- You may postpone your payments up to 2 years considering the type of your loan, amount of total debt, ability to repay, your collateral and credit records.

|

Before-overdue debt management

Before-overdue debt management

| Criteria |

Details of Support |

| Eligibility |

- In order to apply, you need …

- to have debts in two or more financial institutions, and

- debt of which total amount is no more than KRW 1.5 billion, and unsecured debt is no more than KRW 1 billion, while secured debt is no more than KRW 500 million, and

- to have a payment which is less than 31 days overdue or expected to have an overdue payment, and

- newly created(created within 6 months from the application day) debts no more than 30% of the total debt, and

- to have experienced unemployment, leave of absence, closure of business, disease, deterioration of credit etc which made ordinary repayment without DMP difficult, and one of the following should be true.

① The unemployment, leave of absence, or the closure of business happened in the last 6 months.

② In the last one month you were diagnosed with a disease that requires hospitalization for three months or longer.

③ Your credit was deteriorated recently(credit rating equal to or lower than 7th ranking, or overdue period of 1~30 days, or overdue of more than 5 days to have happened more than 2 times within the recent six months)

|

| Interest Rate Reduction |

- The overdue interest is fully exempted.

- During the period of redemption by installment, interest rate is the contracted rate(a maximum of 15.0%, in case of credit cards, a maximum of 10.0%).

- During the period of payment delay, interest rate is the contracted rate(in case of credit cards, a maximum of 10.0%).

|

|

Extension of Repayment period

|

- Period of redemption by equal installment of principal and interest is a maximum of 10 years.

- Payment is delayed for 6 months before the period of redemption by installment.

|

| Postponement of Payments |

- You may postpone your payments up to 2 years considering the type of your loan, amount of total debt, ability to repay, your collateral and credit records.

|

Assistance in Filing for Individual Rehabilitation and Bankruptcy

If you have difficulties in repaying your debt or if you are facing bankruptcy, we help you file for individual rehabilitation and bankruptcy.

- We provide free assistance in preparing necessary documents in filing for individual rehabilitation and bankruptcy, such as application forms and repayment schedule.

- Korea Legal Aid Corporation and our Legal Services Department substitute the legal process.

- Fast Track Agreements with major courts across the country enable simplified and speedy filing processes.

Preferential Treatment Program for Steady Payers

Various incentives are available if you make steady payments according to your repayment schedule for a set period of time. The incentives are as following:

- Early removal of public records from your credit reports

- Emergency Loan for Living Expenses

- Making new credit cards from particular financial institutions